Key Takeaways: Navigating Insurance for Rehab in Ohio

Before you dive in, use this quick assessment to orient yourself in the insurance process:| If your situation is… | Your Immediate Next Step |

|---|---|

| I have private insurance (Anthem, Medical Mutual, etc.) | Call the number on the back of your card to verify “Behavioral Health” benefits. |

| I have Ohio Medicaid (CareSource, Buckeye, etc.) | Search for “Medicaid-certified” facilities in your managed care network. |

| I have no insurance | Contact your local ADAMH Board or ask facilities about sliding scale fees. |

- Top Success Factor: Verification. Never assume coverage; always get written confirmation of benefits before admission.

- Critical Protection: Parity Laws. In Ohio, your insurer cannot legally place stricter limits on addiction treatment than on medical/surgical care.

- Immediate Action: Locate your insurance card and use the script provided in Section 2 to call your provider today.

Understanding Coverage at an Ohio Rehab That Accepts Insurance

Finding an Ohio rehab that accepts insurance can feel like navigating a maze, especially when you or a loved one is in crisis. However, understanding your coverage is the single most effective tool for accessing quality care without financial ruin. Most health plans in Ohio provide significant reimbursement for substance abuse treatment—you just need to know how to unlock those benefits.

Your insurance policy is a contract. It outlines what is covered, what you pay, and who you can see. Thanks to the Mental Health Parity and Addiction Equity Act, insurance companies are required to cover mental health and substance use disorder treatment at levels comparable to medical and surgical care. This means if your plan charges a $50 copay for a cardiologist, they generally cannot charge $100 for an addiction counselor.

To make informed decisions, you must understand these four key terms:

- Deductible

- The amount you pay out-of-pocket before your insurance starts contributing. If your deductible is $1,500, you pay the first $1,500 of treatment costs.

- Copays

- Fixed amounts you pay for specific services (e.g., $30 per therapy session).

- Coinsurance

- The percentage of costs you pay after meeting your deductible. If your plan covers 80%, your coinsurance is the remaining 20%.

- Out-of-Pocket Maximum

- The absolute most you will pay in a year. Once you hit this number, the insurance carrier typically covers 100% of allowed amounts.

Many Ohio treatment centers work with major insurers common in our state—including Medical Mutual, Anthem Blue Cross Blue Shield, CareSource, and Buckeye Health Plan. If you are covered through Ohio’s Medicaid expansion, you have access to comprehensive addiction treatment benefits through these managed care plans.

How Insurance Parity Laws Protect You

Parity laws act as a safety net, ensuring your insurance cannot place tougher rules on rehab than on other health services. The Mental Health Parity and Addiction Equity Act (MHPAEA) mandates that your plan cannot set stricter limits for addiction treatment than for medical care, such as annual visit limits or higher copays5. This protection is vital for anyone seeking an Ohio rehab that accepts insurance because it removes discriminatory barriers to entry.

Mental Health Parity Requirements

Parity rules specifically prevent your plan from imposing “quantitative” limits (like a cap on the number of days in residential treatment) that are more restrictive than those for medical/surgical stays. For example, if your health plan covers unlimited hospital days for a heart condition, it generally cannot put a hard cap on days for substance use disorder treatment.

Action Step: Review your plan’s “Summary of Benefits” document. Compare the “Behavioral Health” section to the “Medical/Surgical” section. If you see a discrepancy—like a visit limit on therapy that doesn’t exist for cardiology—you may have grounds to challenge it based on parity laws.

Essential Health Benefits Under ACA

Under the Affordable Care Act (ACA), all Marketplace plans and many Medicaid plans in Ohio must classify addiction treatment as an “Essential Health Benefit.” This means coverage must include:

- Counseling and psychotherapy

- Inpatient residential rehab

- Outpatient care

- Substance use disorder medication

Crucially, these plans cannot impose yearly or lifetime dollar limits on these essential services1, 2. This ensures that your care is dictated by your recovery progress, not a financial cap.

Types of Insurance That Cover Rehab

Different types of insurance offer different pathways to recovery. Identifying your specific type of coverage is the first step in narrowing down your facility options.

Commercial Plans and Marketplace Options

Commercial insurance—whether provided by an employer or purchased on HealthCare.gov—is a robust bridge to recovery. All Marketplace plans in Ohio must cover mental health and substance use disorder services1. When searching for an Ohio rehab that accepts insurance, commercial PPO plans often offer the most flexibility, allowing you to choose between in-network and out-of-network providers, though out-of-network will cost more.

Ohio Medicaid Expansion Coverage

Ohio’s Medicaid expansion has been a game-changer for access to care. Nearly 770,000 Ohioans are covered by Medicaid expansion, and approximately 40% of these enrollees have a primary mental health or substance use disorder diagnosis3, 4. Medicaid in Ohio covers counseling, inpatient/outpatient rehab, and medication-assisted treatment (MAT). If you have Medicaid, your search should focus specifically on facilities that are “Medicaid-certified” to ensure zero or low out-of-pocket costs.

Verifying Benefits for an Ohio Rehab That Accepts Insurance

Verifying your benefits is the process of confirming exactly what your specific plan covers before you admit to a facility. This step prevents surprise bills later. While many treatment centers (including Arista) offer complimentary benefit verification, knowing how to do it yourself empowers you to make quick decisions.

What to Ask Your Insurance Provider

When you call the customer service number on the back of your card, you need to be specific. General questions get general answers. Use the script below to get the precise data you need.

Script for Insurance Verification: “I am calling to verify my behavioral health benefits for substance use disorder treatment.”

- “Is my plan an HMO or a PPO?”

- “What is my deductible for in-network residential treatment, and how much has been met this year?”

- “What is my copay or coinsurance percentage for inpatient rehab?”

- “Does my plan require Prior Authorization before I can be admitted?”

- “Do I have coverage for out-of-network facilities? If so, what is the deductible?”

Pro Tip: Always write down the date, time, and the name of the representative you spoke with. Ask for a “Reference Number” for the call. This documentation is your proof if a dispute arises later.

Key Questions About Treatment Levels

Addiction treatment isn’t one-size-fits-all; it happens at different “levels of care.” You must confirm which levels your plan covers. Specifically ask about:

- Detoxification: Medical supervision during withdrawal.

- Residential (Inpatient): Living at the facility for 24/7 care.

- Partial Hospitalization (PHP): Day treatment where you go home at night.

- Intensive Outpatient (IOP): Therapy sessions several times a week.

Also, ask specifically about medication coverage. In Ohio, 99% of insured individuals have coverage for Vivitrol, and Suboxone is widely covered10.

Understanding Prior Authorization Rules

Prior authorization is essentially a “permission slip” from your insurance company. Your doctor recommends rehab, but the insurer wants to review the request before agreeing to pay. Research shows that prior authorization rules are a leading barrier to timely substance use treatment in Ohio7. If your plan requires this, the rehab facility will usually handle the paperwork, but you must know about it upfront to avoid delays.

Navigating Common Coverage Barriers

Even with good insurance, you may face “speed bumps.” The two most common are Medical Necessity and Network Restrictions.

Medical Necessity Determinations

Insurance companies only pay for care they deem “medically necessary.” They use specific criteria (often based on ASAM guidelines) to decide if you need inpatient care or if outpatient care is sufficient. If your insurer denies coverage based on medical necessity, you can appeal by providing detailed notes from your doctor explaining why a lower level of care would be unsafe.

Network Restrictions and Out-of-Pocket

Using an in-network Ohio rehab that accepts insurance is almost always cheaper. “In-network” means the facility has a contract with your insurer to charge lower rates. “Out-of-network” means no contract exists, and you may be responsible for the difference between what the provider charges and what the insurance pays (balance billing).

Finding an In-Network Ohio Rehab That Accepts Insurance

Once you understand your benefits, the next step is locating a facility. Ohio offers several state-specific resources to help you locate quality treatment options.

- Ohio Department of Mental Health and Addiction Services: Maintains a provider directory at mha.ohio.gov.

- RecoveryOhio: Provides facility information at recovery.ohio.gov.

- Ohio 211: Dial 2-1-1 from any phone to speak with specialists who can help you find local treatment options.

If you have Ohio Medicaid, remember that the state uses managed care plans (like Buckeye Health Plan, CareSource, and Molina Healthcare), so you must search within your specific managed care network.

Evaluating Treatment Program Quality

Not all rehabs are created equal. When evaluating an Ohio rehab that accepts insurance, look for these quality indicators to ensure you are getting effective care:

| Quality Indicator | Why It Matters |

|---|---|

| Accreditation (JCAHO or CARF) | Ensures the facility meets rigorous national safety and quality standards. |

| ASAM Alignment | The program uses American Society of Addiction Medicine criteria to place you in the correct level of care8. |

| Evidence-Based Therapies | Uses proven methods like CBT, DBT, and Medication-Assisted Treatment (MAT). |

ASAM Criteria and Evidence-Based Care

The ASAM Criteria is the gold standard for matching patients to the right level of care. A quality facility will assess your medical history, withdrawal potential, and living environment before recommending a program. This assessment is often required by insurance companies to prove “medical necessity.”

Specialized Programs for Your Needs

Many Ohio rehab centers offer specialized tracks for veterans, women, LGBTQ+ individuals, or professionals. These programs can make the recovery environment feel safer and more relatable. In Ohio, where nearly 40% of Medicaid expansion enrollees have a dual diagnosis, finding a program that offers specialized mental health support is often critical4.

Maximizing Your Insurance Benefits

To get the most out of your plan, ensure you are utilizing all available benefits, including coverage for medications and co-occurring disorders.

Medication-Assisted Treatment Coverage

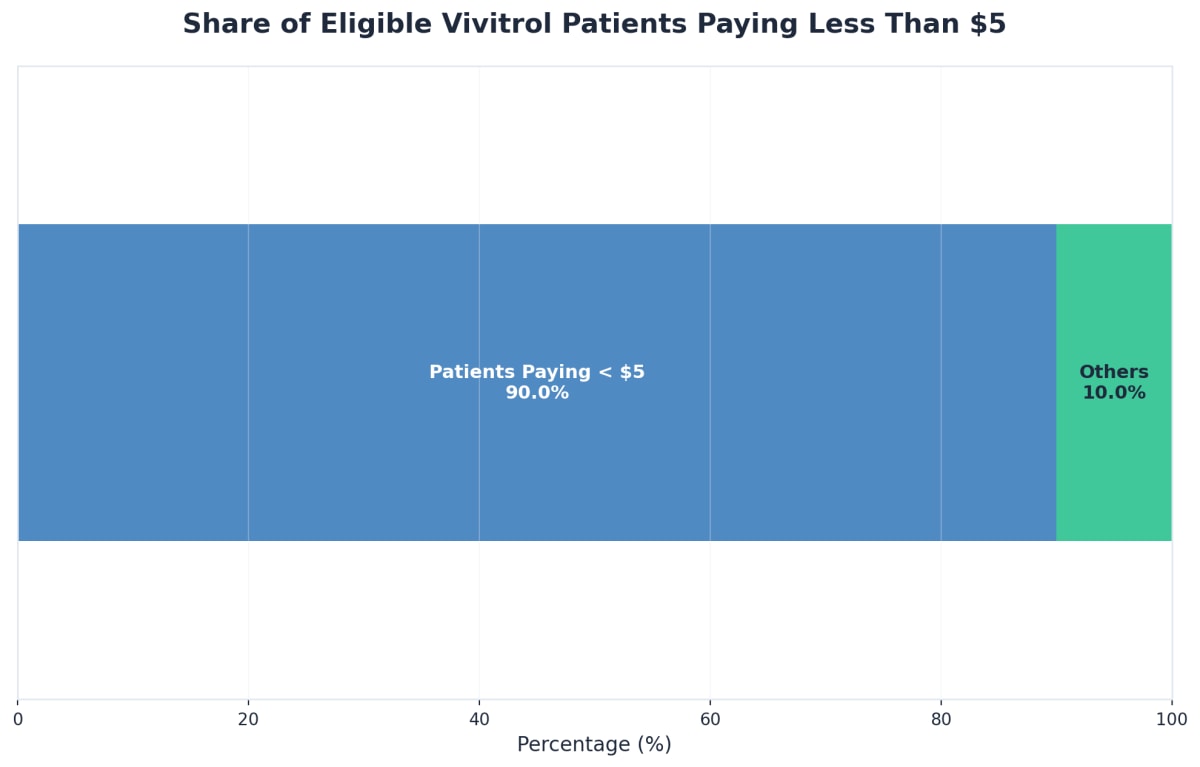

Medication-Assisted Treatment (MAT) combines behavioral therapy with medications like Vivitrol or Suboxone. This is a powerful tool for recovery. In Ohio, coverage for these medications is widespread, with 9 out of 10 insured patients paying less than $5 out-of-pocket for Vivitrol thanks to co-pay assistance programs10.

Coordinating Dual Diagnosis Services

“Dual Diagnosis” refers to treating addiction and a mental health condition (like depression or anxiety) simultaneously. Treating only the addiction often leads to relapse. Most Ohio insurance plans cover coordinated care, but you must confirm that your chosen facility has psychiatrists and licensed mental health counselors on staff to bill for these specific services.

Troubleshooting Insurance Challenges

Even with careful planning, you may encounter roadblocks. Denials and delays are frustrating, but they are often solvable administrative errors rather than final rejections.

When Your Claim Gets Denied

If your insurance denies payment, request a detailed explanation in writing immediately. Denials often stem from missing documentation or incorrect coding. Once you understand the reason, you can work with the facility’s admissions team to file an appeal. Most insurers must respond to urgent appeals within 72 hours.

Understanding Denial Reasons

Common reasons for denial in Ohio include:

- Lack of Medical Necessity: The insurer believes a lower level of care (like outpatient) is sufficient.

- Prior Authorization Missing: The facility did not get approval before you admitted.

- Out-of-Network: The facility is not contracted with your plan.

Knowing the specific reason allows you to target your appeal effectively7.

Filing Effective Appeals

An appeal is essentially asking for a second opinion. To file an effective appeal, gather detailed notes from your doctor or the rehab’s clinical team explaining why the treatment is critical for your safety. Submit this packet before the deadline listed on your denial letter. Many claims in Ohio are overturned when additional clinical evidence is provided.

Alternative Funding Options in Ohio

If insurance falls short, you still have options. Ohio offers robust public resources to ensure financial barriers don’t prevent recovery.

State-Funded Treatment Resources

Ohio receives over $1 billion annually in federal funds to support community-based treatment4. Your local Alcohol, Drug Addiction and Mental Health (ADAMH) Board can connect you to state-funded outpatient and residential programs that offer services on a sliding scale or at no cost.

Payment Plans and Financial Assistance

Many private facilities offer payment plans, allowing you to pay off your deductible or out-of-pocket costs over time. Some also offer scholarships or “charity care” spots. Never be afraid to ask the admissions team, “Do you offer any financial assistance or flexible payment options?”

Frequently Asked Questions

Navigating insurance benefits for recovery services can feel overwhelming. Here are answers to common questions families in Ohio ask about insurance and treatment reimbursement.

Will my insurance cover the full cost of rehab in Ohio?

Most insurance plans in Ohio help cover the cost of addiction treatment, but rarely pay 100% of every expense. Your plan might cover things like therapy, inpatient or outpatient rehab, and medication, but you’ll likely have to pay some out-of-pocket costs like deductibles or copays. With laws like the Affordable Care Act, all Ohio Marketplace and Medicaid plans must include mental health and substance use disorder benefits, and there are no yearly or lifetime coverage limits for these services1, 2. Still, your total cost depends on your specific plan, whether your rehab is in-network, and if services are deemed medically necessary by your insurer.

Does my insurance cover residential treatment programs?

Most major carriers provide some level of reimbursement for residential treatment, including programs for substance use disorders and mental health conditions. The extent of benefits varies based on your specific policy, deductible, and whether the facility has contracted with your carrier. Verification of benefits is the best way to understand your exact entitlements.

What’s the difference between in-network and out-of-network coverage?

Contracted (in-network) facilities have negotiated rates with your carrier, typically resulting in lower expenses you’ll pay directly. Non-contracted (out-of-network) providers may still be reimbursed, but you’ll likely pay higher copays or coinsurance. Some policies don’t reimburse non-contracted care at all, making verification essential before starting treatment.

How long will insurance cover treatment?

Benefit duration depends on medical necessity and your specific policy. Initial authorization might span 7-14 days, with extensions based on ongoing clinical assessments. For instance, you might receive initial approval for 30 days of residential care, then your treatment team submits progress reports for extensions. Your treatment team works with carriers to justify continued care when needed.

What happens when insurance benefits run out?

If your policy reaches its coverage limit, you have several options. Many facilities offer self-pay rates with payment plans, you can transition to a lower level of care that your insurance still covers, or you may qualify for state-funded programs. Discussing financial options early with your treatment facility helps you plan for uninterrupted care.

Does Ohio Medicaid cover addiction treatment?

Yes, Ohio Medicaid covers a comprehensive range of substance use disorder services, including residential treatment, outpatient care, and medication-assisted treatment. Through Ohio’s RecoveryOhio initiative, the state has expanded access to treatment services. If you have Medicaid, verify which facilities are Medicaid-certified providers to ensure full reimbursement.

What are typical out-of-pocket costs for residential treatment?

Out-of-pocket expenses vary widely based on your insurance plan. With in-network coverage, you might pay $500-$3,000 for a 30-day program after meeting your deductible. Out-of-network care can range from $5,000-$15,000 or more for the same period. Self-pay rates at facilities typically range from $10,000-$30,000 per month, though many programs offer sliding scale fees based on income.

What if my claim gets denied?

Denials aren’t final. You have the right to appeal carrier decisions, and many denials are overturned when additional clinical information is provided. Treatment facilities often assist with the appeals process to ensure you receive the care you need.

Are family therapy sessions covered?

Many carriers recognize family involvement as crucial to recovery and reimburse family therapy sessions. Benefit specifics vary, so ask about this during your verification call.

How do I know if a rehab facility in Ohio accepts my specific insurance plan?

To find out if a rehab facility in Ohio accepts your specific insurance plan, start by calling the treatment center directly and ask, “Are you in-network with my insurance?” Have your insurance card ready so you can share your plan details. Most Ohio rehab programs that accept insurance will check benefits for you and explain any out-of-pocket costs. You can also call your insurance provider or use their online directory to search for in-network addiction treatment centers in Ohio.

Can I start treatment immediately while my insurance is being verified?

Many Ohio rehab centers that accept insurance will let you start treatment right away while your insurance is being verified. This is called “admitting with pending insurance”—meaning you can begin care even if final approval isn’t finished yet. It’s common for trusted Ohio treatment programs to work quickly with both your family and your insurance plan to confirm benefits, so you don’t have to wait for help.

What if I lose my job and insurance while I’m in treatment?

If you lose your job and insurance while in treatment at an Ohio rehab that accepts insurance, you still have options. First, ask the treatment center’s staff about continuing coverage—they can help you explore COBRA (which lets you temporarily keep your employer’s plan), switching to an ACA Marketplace plan, or applying for Ohio Medicaid if your income now qualifies.

Are medications like Vivitrol and Suboxone covered by most insurance plans in Ohio?

Yes, most insurance plans in Ohio—including Medicaid, commercial insurance, and ACA Marketplace plans—cover medications like Vivitrol (naltrexone) and Suboxone (buprenorphine/naloxone) for addiction treatment. In fact, 99% of people with any type of insurance in Ohio, including Medicaid, have coverage for Vivitrol10.

What should I do if the only quality rehab that fits my needs is out-of-network?

If the only quality rehab that matches your needs is out-of-network, don’t give up. Start by asking your insurance if they’ll approve a “single case agreement” for that specific Ohio rehab that accepts insurance. Sometimes, insurers make exceptions if no in-network center offers the care you need, especially for specialized treatment.

Can my family help me understand my insurance benefits if I’m too overwhelmed?

Yes, your family can absolutely help you understand your insurance benefits if you’re feeling overwhelmed. In Ohio, it’s common for loved ones to get involved by calling your insurance provider together, reading through benefit summaries, or helping organize paperwork. Arista encourages families to work together and offers guidance too.

Will using my insurance for addiction treatment affect my future coverage or premiums?

Using your insurance for addiction treatment at an Ohio rehab that accepts insurance will not cause your insurer to drop you or raise your premiums just because you sought help. Thanks to the Affordable Care Act, insurance companies in Ohio can’t deny you coverage or charge you more based on your history of needing substance use disorder treatment1.

What free resources are available in Ohio if I don’t have insurance?

If you don’t have insurance, Ohio still offers several free and low-cost resources. Start by contacting your local Alcohol, Drug Addiction and Mental Health (ADAMH) Board. You can also call the SAMHSA National Helpline (1-800-662-HELP), a free and confidential service that links you to local treatment options across Ohio6.

How does the recent change in ACA subsidies affect my ability to afford rehab coverage?

Recent changes to ACA subsidies—set to take effect in 2026—are likely to make health insurance on the Marketplace more expensive for many Ohio families. If you rely on ACA Marketplace coverage for rehab, this could mean higher monthly premiums. The end of enhanced subsidies may push some Ohioans to consider Medicaid or state-funded programs for addiction treatment if Marketplace costs rise too much9.

Does insurance cover family therapy and aftercare services in Ohio?

Yes, most insurance plans in Ohio—including Medicaid, private insurance, and Marketplace options—typically cover family therapy and aftercare services as part of addiction treatment. Family therapy is considered an essential benefit under the Affordable Care Act, and many Ohio plans recognize that involving loved ones strengthens recovery outcomes1, 2.

Your Path to Recovery Starts Here

Understanding your insurance benefits removes one of the biggest barriers to treatment—but the most important step is actually reaching out for help. Taking that first step toward recovery can feel overwhelming, but you don’t have to face it alone. Whether you’re struggling with substance use, mental health challenges, or both, compassionate support is available right here in Ohio. Recovery is possible, and it begins with connecting to the right resources.

When choosing a treatment facility, look for programs that offer personalized care plans tailored to your specific needs and circumstances. Quality facilities should provide a full continuum of care—from medical detox through residential treatment, partial hospitalization, intensive outpatient programs, and aftercare support. This allows you to transition smoothly between levels of care as your recovery progresses, without having to start over with a new treatment team.

Arista Recovery’s Ohio-based facilities offer this comprehensive approach to treatment, and our admissions team is available to answer your questions about our programs. Remember, our team can help verify your benefits and explain your coverage options at no cost. Don’t wait another day to explore your options—reach out today to learn how we can support you or your loved one on the path to recovery.

References

- Mental Health & Substance Abuse Coverage – Healthcare.gov. https://www.healthcare.gov/coverage/mental-health-substance-abuse-coverage/

- Substance Use Disorders Resources – Medicaid. https://www.medicaid.gov/medicaid/benefits/behavioral-health-services/substance-use-disorders

- Ohio Section 1115 Demonstration for Substance Use Disorder Treatment. https://medicaid.ohio.gov/resources-for-providers/bh/sud-1115-sub/sud-1115

- Access to Mental Health and Substance Use Disorder Treatment – Health Policy Institute of Ohio. https://www.healthpolicyohio.org/our-work/publications/access-to-mental-health-and-substance-use-disorder-treatment

- New Mental Health and Substance Use Disorder Parity Rules – U.S. Department of Labor. https://www.dol.gov/agencies/ebsa/laws-and-regulations/laws/mental-health-parity/new-mhpaea-rules-what-they-mean-for-providers

- SAMHSA National Helpline – Treatment Referral and Information Service. https://www.samhsa.gov/find-help/helplines/national-helpline

- Insurance Barriers to Substance Use Disorder Treatment – PMC/NIH. https://pmc.ncbi.nlm.nih.gov/articles/PMC9948907/

- About The ASAM Criteria – American Society of Addiction Medicine. https://www.asam.org/asam-criteria/about-the-asam-criteria

- 4 Big Changes from One Big Beautiful Bill Act – American Medical Association. https://www.ama-assn.org/health-care-advocacy/federal-advocacy/4-big-beautiful-bill-changes-will-reshape-care-2026

- Verifying Insurance Benefits for VIVITROL® – VIVITROL. https://www.vivitrol.com/opioid-dependence/verify-insurance-coverage